|

|

Time series data is ubiquitous in various fields such as finance, meteorology, medicine, and more. Detecting significant changes in time series data is crucial for understanding underlying patterns and making informed decisions. However, it is equally important to determine when these changes are no longer significant. This article delves into the technical aspects of detecting significant changes in time series data and how to ascertain when these changes cease to be significant. Table of Content

Understanding Change Point DetectionChange point detection (CPD) is a technique used to identify points in time where the statistical properties of a time series change abruptly. These changes can manifest in various forms, such as shifts in mean, variance, correlation, or spectral density. CPD is essential for applications like quality control in manufacturing, climate change analysis, and medical condition monitoring. Types of Change Points

Methods for Change Point DetectionSeveral methods have been developed for detecting change points in time series data. These methods can be broadly categorized into offline and online techniques. 1. Offline Change Point DetectionOffline methods analyze the entire time series data to identify change points. These methods are suitable for post hoc analysis and often provide more accurate estimations of change points.

2. Online Change Point DetectionOnline methods detect change points in real-time as new data becomes available. These methods are crucial for applications requiring immediate detection of changes.

Threshold Selection Strategies for Detecting Significant ChangesSelecting an appropriate threshold for detecting significant changes is crucial. This threshold can be fixed or adaptive, depending on the nature of the time series.

Evaluating the Significance of Change PointsOnce change points are detected, it is essential to evaluate their significance. This involves determining whether the detected changes are statistically significant or merely due to random fluctuations. Statistical Tests:

Detecting When Changes Are No Longer SignificantDetermining when changes in time series data are no longer significant involves monitoring the time series for periods of stability. This can be achieved through various techniques: 1. Moving Window AnalysisA moving window analysis involves calculating statistical properties over a sliding window of fixed length. By comparing these properties across different windows, one can identify periods of stability.

2. Control ChartsControl charts are graphical tools used to monitor the stability of a process over time. They plot the time series data along with control limits, which are typically set at ±3 standard deviations from the mean.

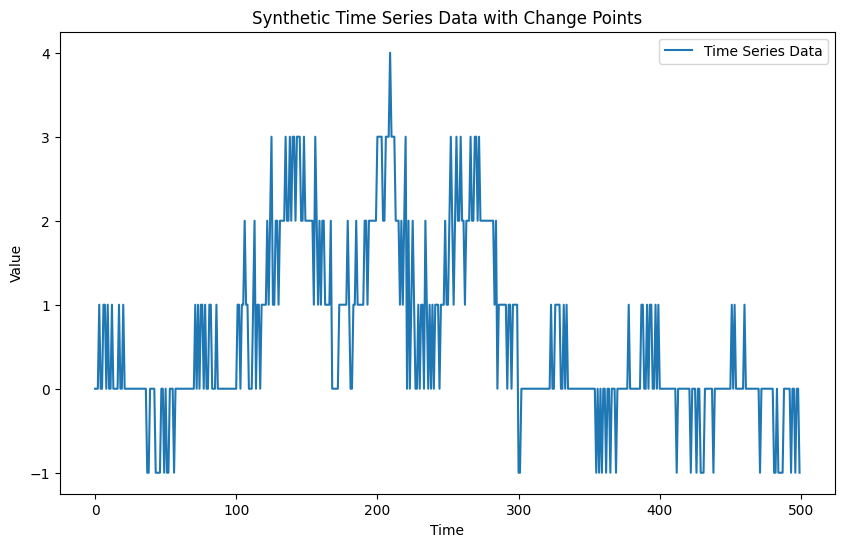

Practical Implementation: Detecting When Changes in Time Series Data Are No Longer SignificantDetecting significant changes in time series data is a crucial task in various fields such as finance, healthcare, and climate science. However, it is equally important to determine when these changes are no longer significant. This practical implementation will guide you through the process using Python, focusing on change point detection and evaluating the significance of these changes. Step 1: Install and Import Necessary Libraries !pip install rupturesFirst, we need to import the necessary libraries for time series analysis and change point detection. Step 2: Generate or Load Time Series Data For this example, we will generate synthetic time series data with known change points. Output: Time Series Data Step 3: Detect Change Points We will use the ruptures library to detect change points in the time series data. Output:  Detect Change Points Step 4: Evaluate the Significance of Change Points To evaluate the significance of the detected change points, we can use statistical tests such as the Augmented Dickey-Fuller (ADF) test to check for stationarity. The p-values below 0.05, indicates that the null hypothesis of non-stationarity can be rejected. This means that each segment is stationary, and the detected change points are significant. Output: Segment 1:

ADF Statistic: -2.210469

p-value: 0.202468

Critical Values:

1%, -3.661428725118324

Critical Values:

5%, -2.960525341210433

Critical Values:

10%, -2.6193188033298647

Segment 2:

ADF Statistic: -3.434827

p-value: 0.009827

Critical Values:

1%, -3.639224104416853

Critical Values:

5%, -2.9512301791166293

Critical Values:

10%, -2.614446989619377

Segment 3:

ADF Statistic: -3.929395

p-value: 0.001829

Critical Values:

1%, -4.223238279489106

Critical Values:

5%, -3.189368925619835

Critical Values:

10%, -2.729839421487603

Segment 4:

ADF Statistic: -6.412650

p-value: 0.000000

Critical Values:

1%, -3.639224104416853

Critical Values:

5%, -2.9512301791166293

Critical Values:

10%, -2.614446989619377

Segment 5:

ADF Statistic: -5.653803

p-value: 0.000001

Critical Values:

1%, -3.639224104416853

Critical Values:

5%, -2.9512301791166293

Critical Values:

10%, -2.614446989619377

Segment 6:

ADF Statistic: -4.740883

p-value: 0.000070

Critical Values:

1%, -3.4615775784078466

Critical Values:

5%, -2.875271898983725

Critical Values:

10%, -2.5740891037735847Step 5: Detect When Changes Are No Longer Significant To detect when changes are no longer significant, we can use a moving window analysis to monitor the stability of the time series. We performed a moving window analysis to monitor the stability of the time series. The moving average and moving standard deviation were calculated using a window size of 50. Output:  Detect When Changes Are No Longer Significant The moving average remains relatively stable, with noticeable shifts at the change points.

The mean standard deviation line helps to identify periods of stability. When the moving standard deviation is close to the mean standard deviation, it indicates that the time series is stable and changes are no longer significant. ConclusionDetecting significant changes in time series data and determining when these changes are no longer significant are critical tasks in various fields. By leveraging techniques such as moving window analysis, control charts, and statistical tests, one can effectively monitor time series data for periods of stability. Despite the challenges, ongoing research and advancements in change point detection methods continue to improve our ability to analyze and interpret time series data. |

Reffered: https://www.geeksforgeeks.org

| AI ML DS |

Type: | Geek |

Category: | Coding |

Sub Category: | Tutorial |

Uploaded by: | Admin |

Views: | 17 |