|

Teaching kids about interests in mathematics is a challenging task. First start with the basics: “Interest is extra money you get for lending your money or extra money you pay for borrowing money.”

Introduce the key elements:

- Principal: Original amount of money

- Rate: Percentage of interest charged or earned

- Time: How long the money is borrowed or lent

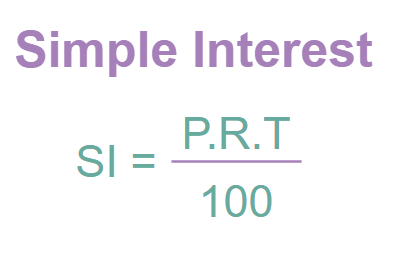

Use Simple Interest Formula: Simple Interest = (Principal × Rate × Time), where the rate is in decimals. The simple interest formula is added below:

Provide an example: “Imagine you save $100 in a bank. The bank offers 5% interest per year. After one year, you’ll earn: Interest = $100 × 0.05 × 1 = $5”

Show how the money grows: “Your new total would be $105 ($100 + $5)”

Introduce compound interest: “If you leave the money for another year, you’ll earn interest on $105, not just $100”

Magic of Compound Interest

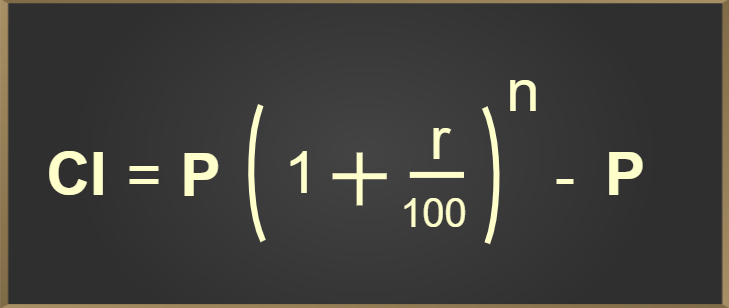

“Compound interest is when you earn interest not just on your original money, but also on the interest you’ve already earned.” The compound Interest formula is added below:

Snowball effect: “It’s like rolling a snowball down a hill. As it rolls, it picks up more snow, getting bigger and bigger faster and faster.”

Example: Let’s say you save $100 and earn 10% interest each year:

- After 1 year: $110 ($100 + $10 interest)

- After 2 years: $121 ($110 + $11 interest)

- After 3 years: $133.10 ($121 + $12.10 interest)

Comparison with Simple Interest: “With simple interest, you’d only have $130 after 3 years. Compound interest gives you more!”

Power of time: “The longer you leave your money, the more dramatic the effect becomes.”

Visual Representation: Consider drawing a graph showing how money grows with compound interest versus simple interest over time.

Real-Life Application: “This is why starting to save early, even with small amounts, can lead to big results later in life.”

Activities to Teach Kids About Compound Interest

Various activities to teach kids about compound interest includes:

- Magic Penny: Ask the child if they’d prefer $1 million now or a penny that doubles every day for 30 days. Calculate together how the penny grows, showing how small amounts can become large through compounding.

- Savings Jar Game: Use a clear jar and small objects (like beans). Add a set number each day, plus extra to represent interest. This visually shows growth over time.

- Interest Snowball: Draw a small snowball on paper. Each “year,” draw a bigger snowball around it, representing how money grows with compound interest.

- Chocolate Chip Math: Use chocolate chips to represent money. Add more chips as “interest” each round, then eat the extra as a reward!

- Online Compound Interest Calculator: For older kids, use a simple online calculator to play with different scenarios.

Teacing Interest Using Games

Students can learn about Interest using various games that are added below:

- Interest Tag: Players are “money” and one player is “interest.” When tagged, players join hands with “interest,” forming a growing chain. This shows how interest makes money grow.

- Compound Interest Monopoly: Modify Monopoly rules. When players pass GO, they get interest on their current money in addition to the usual $200.

- Interest Dice: Roll dice to determine initial savings and interest rate. Use these numbers in simple calculations to see who can grow their money the most in a set number of turns.

- Bank Teller Role-Play: Kids play bank tellers, calculating interest for “customers” using play money and simple interest charts.

- Interest Rate Race: Set up a board game where players move based on different interest rates. Higher rates let players move faster, demonstrating the impact of interest rates on growth.

- Savings Challenge: A longer-term game where kids track their pretend savings over weeks, adding “interest” regularly. The one with the most at the end wins.

- Computer Interest Game: For tech-savvy kids, there are simple online games that simulate saving and earning interest over time.

Also, you ae advice to ask students to solve various questions of interest that are added below:

Practice Questions on Simple Interest

Question 1: What is the simple interest on $5000 at 4% per annum for 3 years?

Solution:

- Principal (P) = $5000

- Rate (r) = 4% = 0.04

- Time (t) = 3 years

Using the formula: I = P × r × t

I = 5000 × 0.04 × 3

I = $600

Simple interest is $600.

Question 2: John borrowed $2000 from a bank at 5% simple interest per annum. How much will he owe after 2 years?

Solution:

- P = $2000

- r = 5% = 0.05

- t = 2 years

Interest (I) = P × r × t = 2000 × 0.05 × 2 = $200

Total amount = Principal + Interest = $2000 + $200 = $2200

John will owe $2200 after 2 years.

Question 3: A sum of money becomes $1800 in 2 years at 5% simple interest per annum. What was the original sum?

Solution:

Let the original sum be P

- Rate (r) = 5% = 0.05

- Time (t) = 2 years

- Amount (A) = $1800

Using the formula: A = P + P × r × t

1800 = P + P × 0.05 × 2

1800 = P + 0.1P

1800 = 1.1P

P = 1800/1.1 = $1636.36

Original sum was $1636.36.

Question 4: In how many years will $600 amount to $750 at 5% simple interest per annum?

Solution:

- P = $600

- A = $750

- r = 5% = 0.05

Let the time be t years

Using A = P + P × r × t

750 = 600 + 600 × 0.05 × t

150 = 30t

t = 150/30 = 5 years

It will take 5 years

Practice Questions on Compound Interest

Question 1: Calculate the final amount if $5000 is invested at 6% per annum compounded annually for 3 years.

Solution:

Using formula A = P(1 + r/n)(nt)

Where, P = $5000, r = 0.06, n = 1 (annually), t = 3

A = 5000(1 + 0.06/1)(1×3)

A = 5000(1.06)3

A = 5000 × 1.191016

A = $5955.08

Final amount after 3 years will be $5955.08.

Question 2: How much interest is earned on $10,000 invested at 8% per annum compounded quarterly for 2 years?

Solution:

Using A = P(1 + r/n)(nt)

Where, P = $10,000, r = 0.08, n = 4 (quarterly), t = 2

A = 10000(1 + 0.08/4)(4×2)

A = 10000(1.02)8

A = 10000 × 1.171659

A = $11,716.59

Interest earned = Final amount – Principal

= $11,716.59 – $10,000 = $1,716.59

Question 3: What principal amount should be invested at 5% per annum compounded semi-annually to get $10,000 after 4 years?

Solution:

We need to use the formula A = P(1 + r/n)(nt) and solve for P

Where, A = $10,000, r = 0.05, n = 2 (semi-annually), t = 4

10000 = P(1 + 0.05/2)^(2×4)

10000 = P(1.025)8

10000 = P × 1.21899

P = 10000/1.21899

P = $8203.45

Principal amount should be $8203.45.

Question 4: Calculate the time required for $2000 to double at 8% per annum compounded monthly.

Solution:

We can use the Rule of 72 for a quick approximation:

Time to double ≈ 72 / (r × 100), where r is the interest rate as a percentage

≈ 72 / 8 = 9 years

For a more precise calculation:

Using A = P(1 + r/n)^(nt), where A = 2P (double the principal)

2P = P(1 + 0.08/12)^(12t)

2 = (1 + 0.08/12)^(12t)

ln(2) = 12t × ln(1 + 0.08/12)

t = ln(2)/(12 × ln(1.006667))

t = 8.76 years

Exact time required is 8.76 years.

Read More:

Frequently Asked Questions

What is Compound Interest?

Compound interest is interest calculated on both the initial principal and the accumulated interest from previous periods.

How is Compound Interest Different from Simple Interest?

Compound interest grows exponentially as it earns interest on interest, while simple interest grows linearly based only on the principal.

What Factors Affect Compound Interest Calculations?

Factors that affect Compound Interest Calculations are, principal amount, interest rate, compounding frequency, and time period.

What is Rule of 72?

A quick way to estimate how long it takes money to double at a given interest rate. Divide 72 by the interest rate percentage.

Is Compound Interest Good for Borrowers?

Generally speaking No. For borrowers, compound interest can make debts grow faster, especially if payments are missed or delayed.

|